2024-02-29

This is a new series that i will start where i will first go over the basic or “relative” basic of options in this post and then in each new post will go over certain options strategys beginning with beginner then intermediate and at the end advanced.

0 DTE options expire on the same day as they start trading. A 0DTE option could be an option that is only listed for a single day or a longerterm option that reached its last day of trading. 46% of the total trading volume is equities options is in options with a expiration less than 5 days (5DTE). 0DTE options are mostly used for market participants that play one-day moves in indices like the SPX, SPX or some ETFs. Most of the time they are used for naked OTM calls or naked OTM puts trying to get intraday moves. This is a low probability approach of winrate but can produce big returns with a low risk on a risk to reward basis.

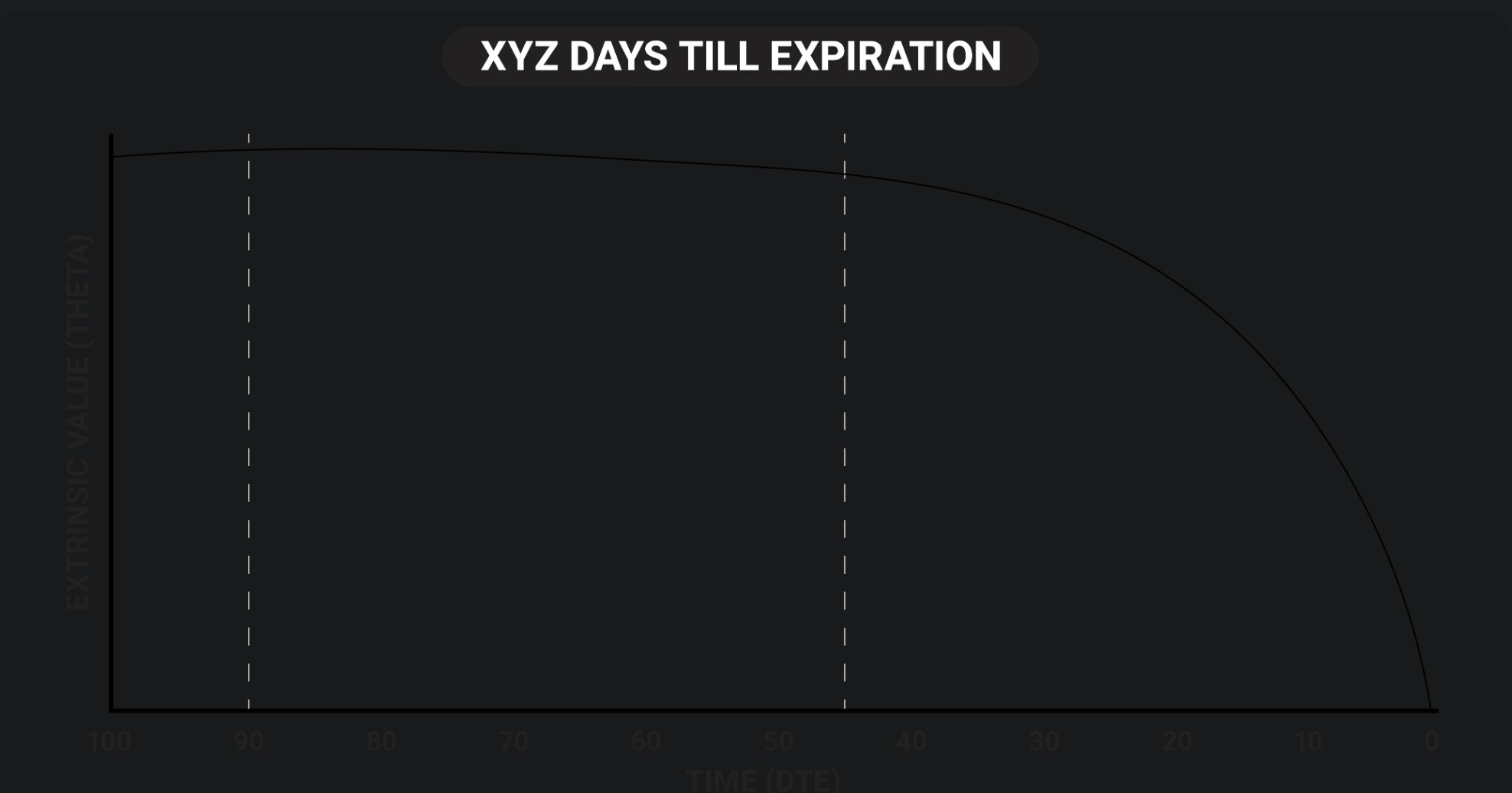

The Theta (i will go over the greeks in a later post) of Options is the factor at which the price of a option will decay each day. For example a 1$ 5DTE option might have a theta of 0.2$ so the price will decrease 0.2$ per day. So for a 0DTE option the theta or extrinsic value of the option decays in a single day.

The DTE are completly dependent on your style of trading it aslways weighting risk vs reward. There is some evidence that suggest that 45DTE might be the best option for short term trading. There are 2 factors where it comes to optimizing trade duration “theta decay” “time to be correct”.

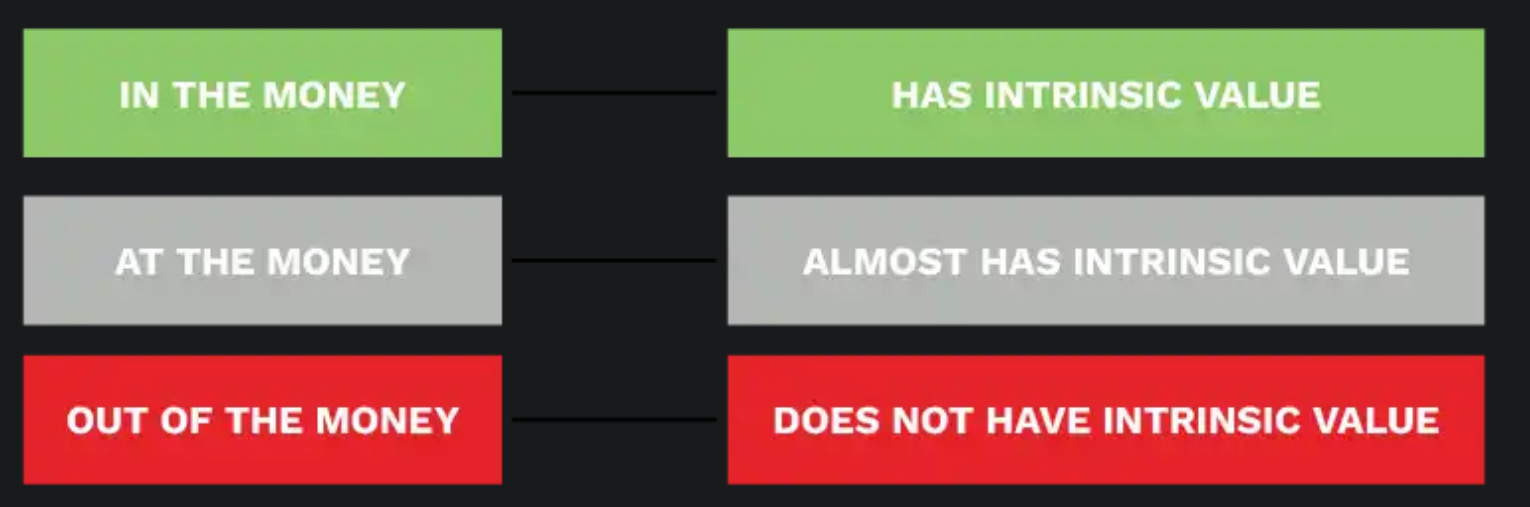

Assignment reffers to when the obligations of an options contract are fulfilled, this happens when an holder of the options exercises their rights. The OCC (clearing house) will then randomly assign a excercise notice to a option writer. Option writer should always be prepared to assignment or buying back the underlying at the strike price. Its a zero sum game. Options will most likley be assgined when its is In-the-money or near expiration

Writing a Call Option: This process involves selling someone the right to buy a security from you at a specified price (the strike price) before the option expires.

Writing a Put Option: This process involves selling someone the right to sell a security to you at a specified price before the option expires.

Process:

Option Exercise: The holder of the option (the investor who purchased the option) decides to exercise the option.

Notification: When the option is exercised, the Options Clearing Corporation (OCC) is notified and looks for clients the have sold and option contract of the same series.

Assignment:The selected option writer (the investor who sold the option) is then assigned by the brokerage.

Fulfillment: If it was a call option that was exercised, the assigned writer must sell the underlying asset to the option holder at the agreed-upon strike price. If it was a put option that was exercised, the assigned writer must buy the underlying asset from the option holder at the strike price.

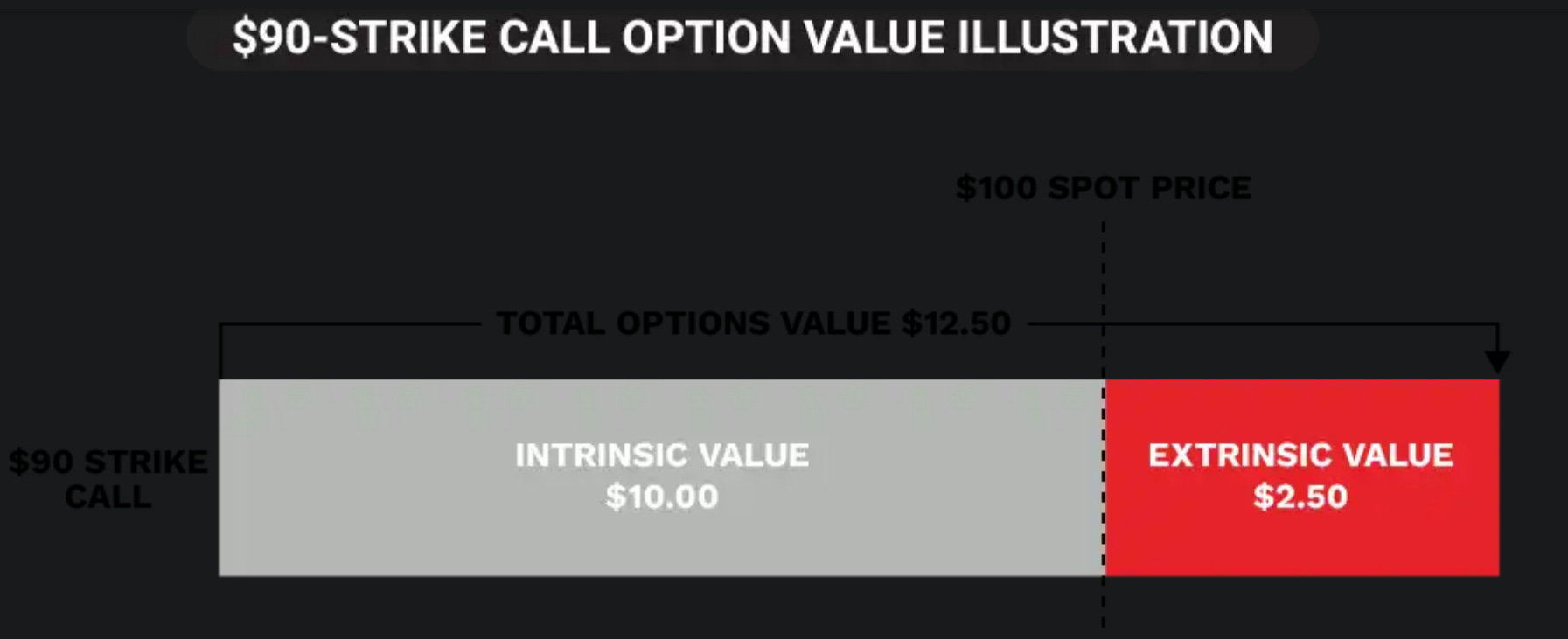

Extrinsic + Intrinsic Value = premium of an option

Intrinsic Value for a ITM option is the difference between the strike price and the stock price, for OTM options it is 0. Extrinsic is the term used for the value of an option beyond its intrinsic value.

The Extrinsic value is influenced by:

Time to Expiration: The more time an option has until it expires, the greater the chance that it could become ITM. Therefore, options with a longer time until expiration have more extrinsic value than options that are closer to expiration.

Implied Volatility: If the underlying asset's price is volatile, there's a greater chance that the option could become ITM. Therefore, options on more volatile assets usually have more extrinsic value.

Interest Rates and Dividends: Changes in interest rates and expected dividends can also influence an option's extrinsic value. Higher interest rates generally increase the extrinsic value of call options and decrease the extrinsic value of put options. Expected dividends generally decrease the extrinsic value of call options and increase the extrinsic value of put options.

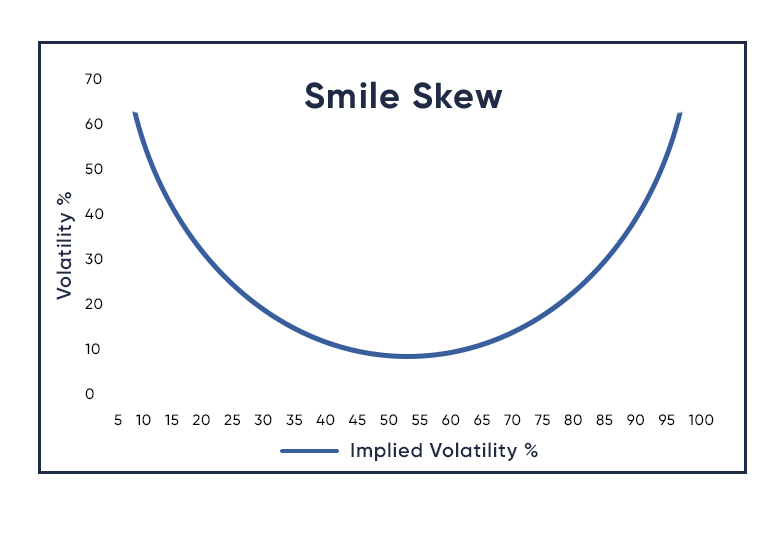

An Option can become intrinsic value if the options moves from OTM to ITM, and the extrensic value gets higher when the option is ATM due to higher uncertainty. THis is why extensic value will drecrease the further we move ITM. THis uncertainty pattern is known as “volatlity smile”

Looking at an example, imagine you have a call option with a strike price of $50, and the underlying stock is currently priced at $55. The market value of the option is $7.

First, calculate the intrinsic value: $55 (underlying price of the stock) - $50 (strike price) = $5.00.

Next, calculate the extrinsic value: $7 (option market price) - $5 (intrinsic value) = $2.00.

Therefore, in this example, the extrinsic value of the option is $2.00.

Options, futures, and futures options only exist through their expiration date, after which these contracts are invalid. Time until expiration may also be referred to as “days-to-expiration,” or DTE. In equity options there are 3 types of options weeklys, monthlys and Long-Term Equity Anticipation Securities (LEAPS). SPX or SPY even offer daily expiration. Monthlies expire on the thrid friday of the month st 3:00 pm CST, if this is a holiday it will expire on the day before. Weeklys are introdued on thrusdays and will expire 8 days later on the friday. THey are only availabe in expiration ranges fronm one to five weeks. while montlys 0 to 11 months. Option with longer than one year expirations are called LEAPS they aswell expire on the third friday of the contract month.

Because options have a finite life, traders basically have two choices when it comes to the trade management of any given position. The trade can be left on until it expires, or it can be closed at some point prior to expiration. A study by tastylive revealed that a 45DTE has the best risk reward

Options pricing models are essential tools used by traders and investors to estimate the value (aka premium) of options.

The most well-known options pricing model is the Black-Scholes model, which provides formulas to calculate the theoretical price of an option based on factors like the current asset price, strike price, time to expiration, volatility, and the risk-free interest rate.

In addition to the Black-Scholes model, some market participants use the Binomial Options Pricing Model (BOPM), or Monte Carlo Simulations. However, both of these latter models require additional effort, mathematical skill, and computational resources.

Different models exist because options can have varying characteristics, and market conditions can fluctuate. Moreover, a single model can’t necessarily capture all the nuances of option pricing across a wide range of scenarios and market environments.

As a result, some market participants employ several different pricing models for specific types of options, situations, and/or market dynamics. In many cases, these models are proprietary, and not available to the public.

It should be noted that the real-world price of an option (e.g. the open market price) may differ from the theoretical value generated by an options pricing model. This may be due to a limitation of the pricing model, or due to a real-world factor in the options market, such as a disruption to supply/demand, an inefficient bid-ask spread, or some other factor.

Such disruptions can develop during severe market corrections, or periods of significant uncertainty, but may also arise in other market environments, for a variety of reasons.

Regardless, the output of an options pricing model - the theoretical value - often serves as a key reference point, and is typically used to evaluate (or compare against) the open market price of an option.

In the options universe, the term “moneyness” refers to the relationship between the current price of the underlying asset and the strike price of the option.

As a reminder, the strike price is the price at which the option holder can buy (for a call option) or sell (for a put option) the underlying asset.

Moneyness is typically categorized in three different ways, in-the-money (ITM), at-the-money (ATM) or out-of-the-money (OTM).

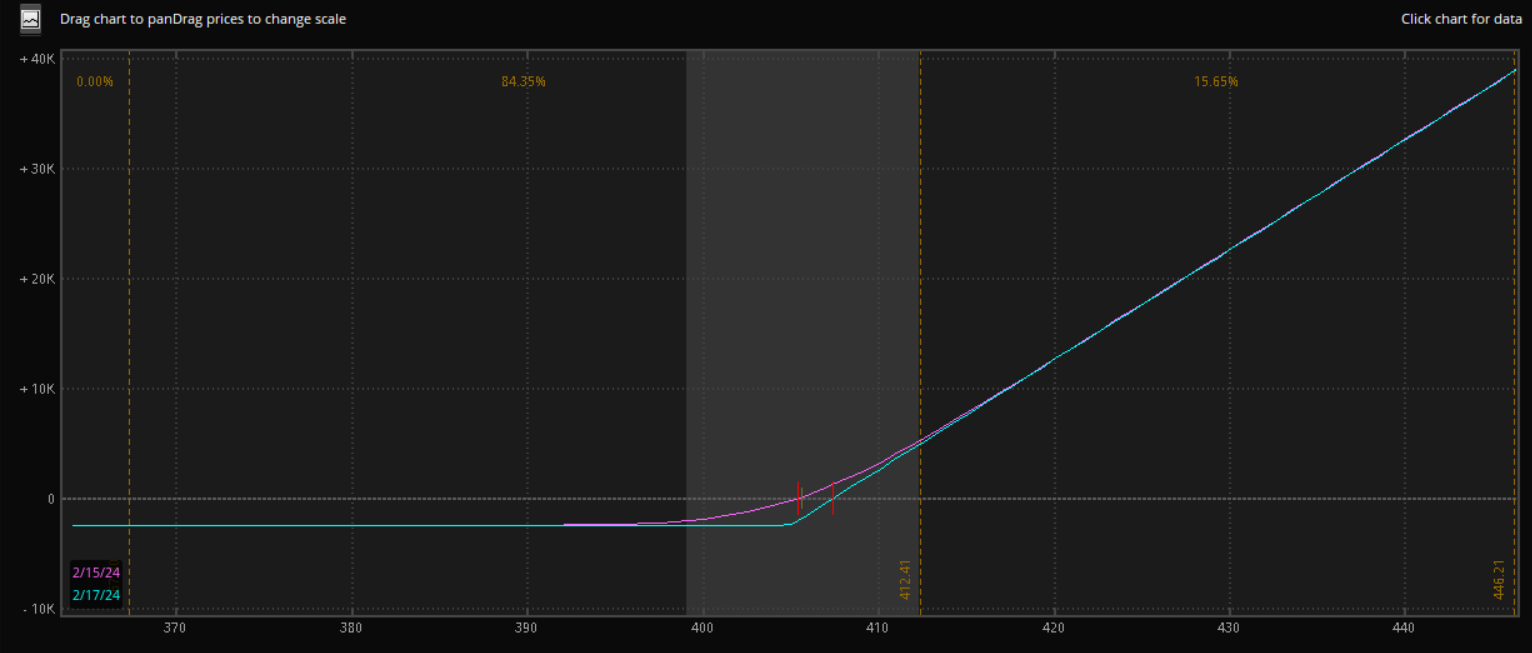

A long call is the most basic option, you have the right to purchase 100 shares of the stock at experiation for the strike price. The stock price needs to be above to strike price to be In-the-money. You have no obligation to exersise your right to buy the shares but the seller of the option has to provide the shares (assignment) to you if the price is above the strike price. Your profit is unlimited and your loss is capped to what you payed for the option (premium)

Long MSFT Call / x-axis strike y-axis profit

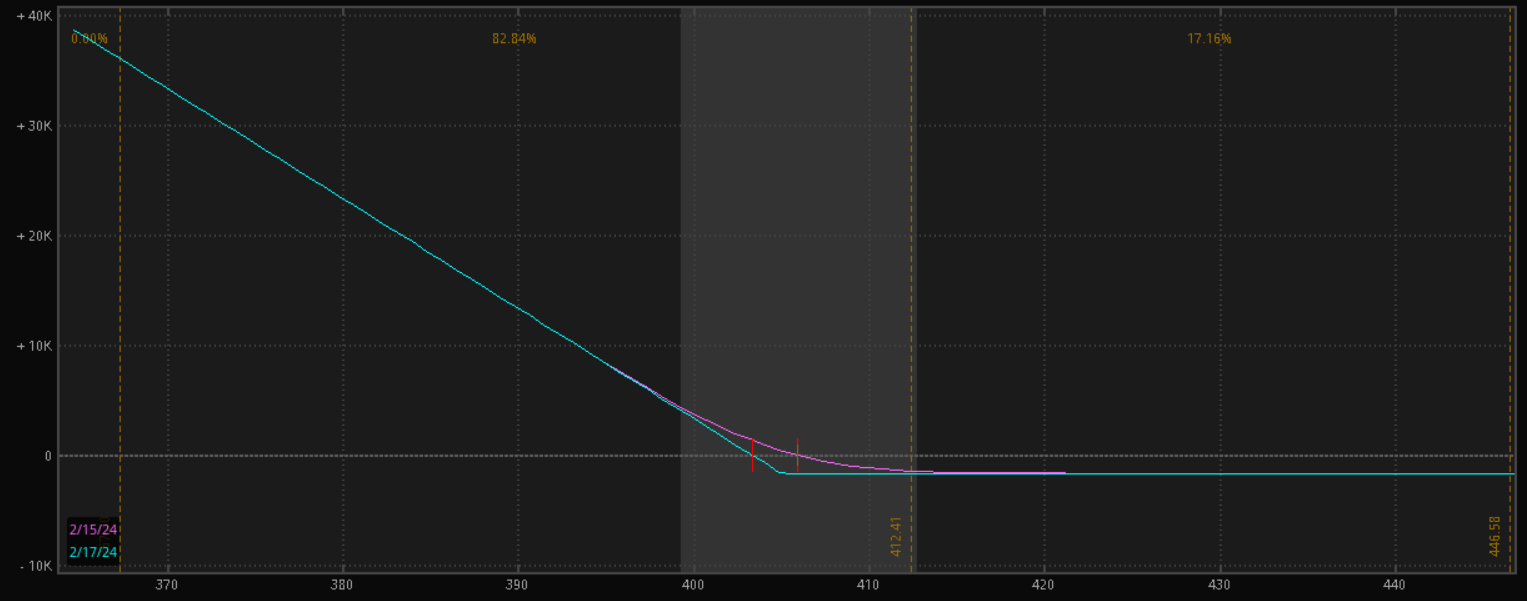

A Long Put is the same as the Long Call just just the other way around so that you bet on the decline of the stock

Longs MSFT Short

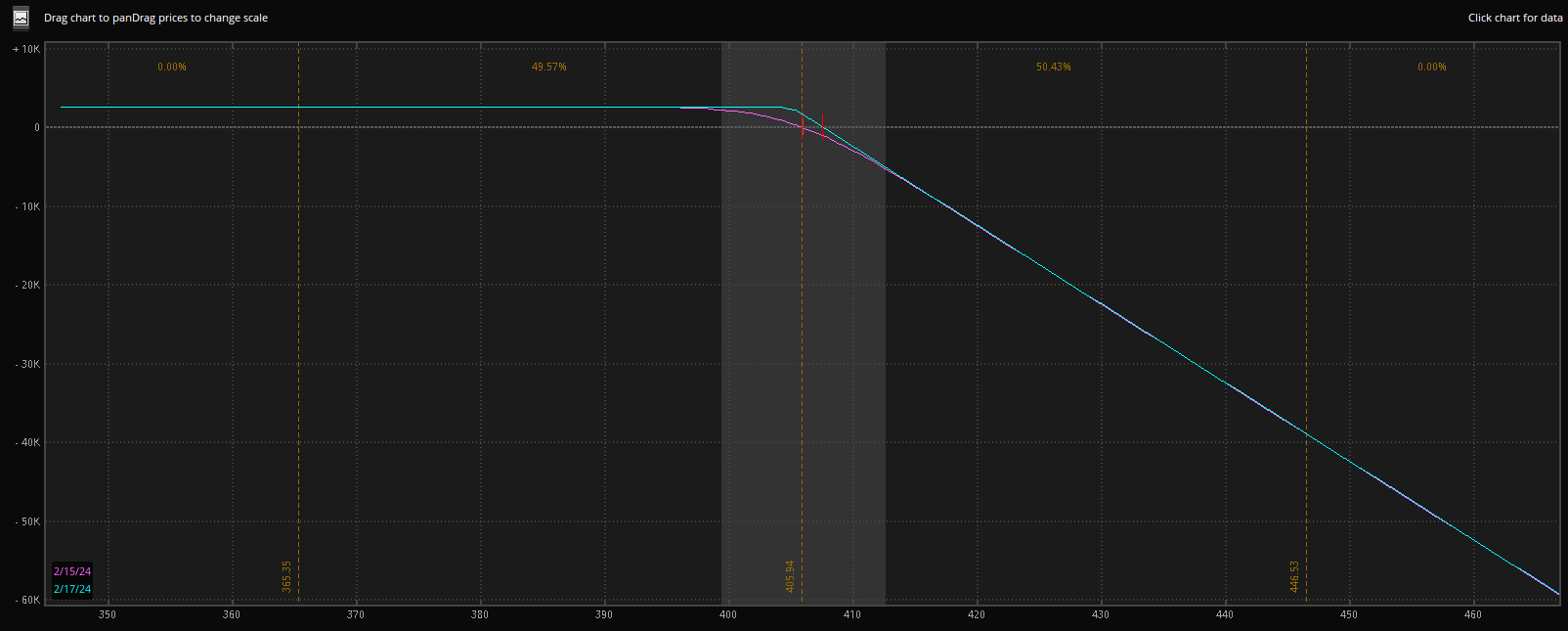

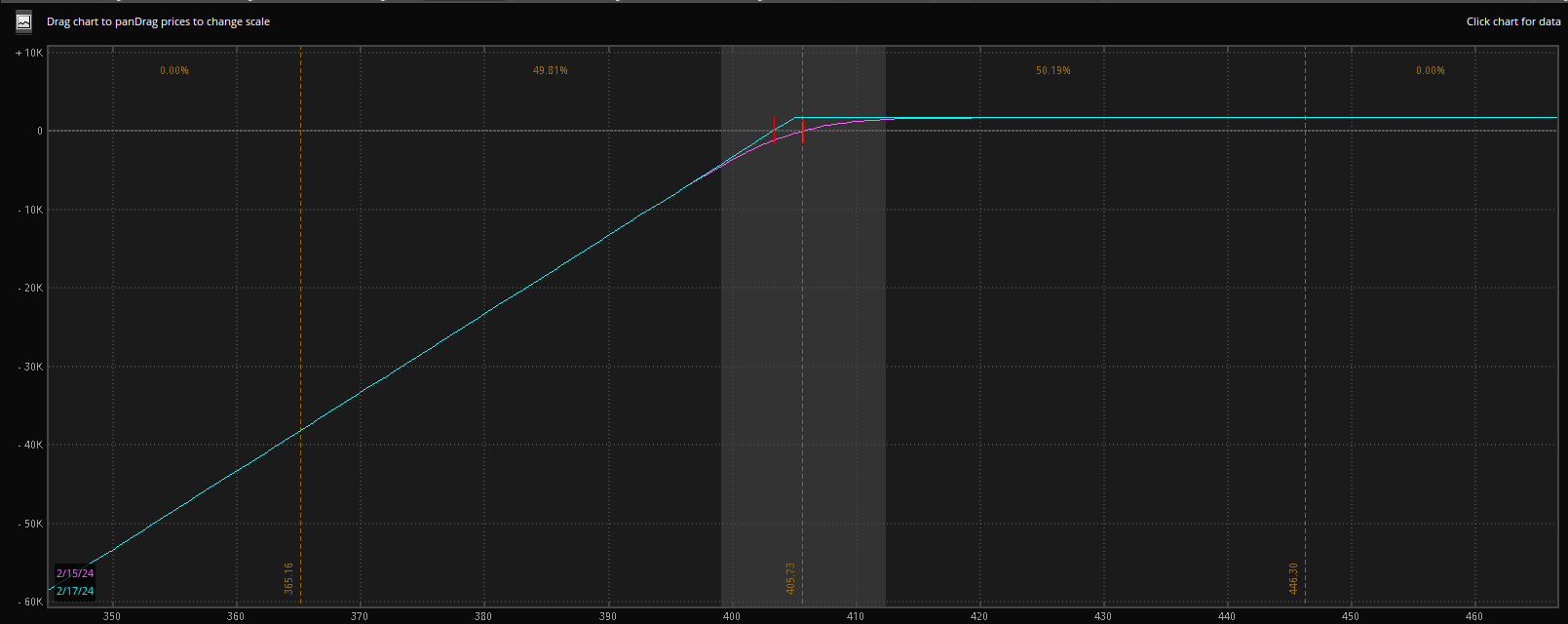

Shorting or writing option is the complete opposide of their long counterparts. You recieve the premium upfront when selling a call and put but aswell have a unlimited loss potential. You can compare it to selling insurance

Short Call MSFT

Short Put MSFT

Thanks,

Finn